The eCommerce fraud detection market will reach $102.28 billion within the next two years, highlighting the escalating challenge of fraudulent activity in online retail. With fierce competition, retailers must avoid scammers continuously refining their tactics to exploit vulnerabilities.

In 2024, retailers faced substantial losses, with $103 billion lost to fraudulent returns and claims—about 15% of the projected $685 billion in returns last year. Given these statistics, fraud prevention strategies are essential to protect operations, enhance customer trust and ensure a secure and positive shopping experience, catering to the expectations of speed, convenience, and ease that today’s online consumers demand.

What Is Ecommerce Fraud?

eCommerce fraud encompasses various malicious activities aimed at exploiting online retailers. This type of fraud ranges from the most common threats, such as fraudulent transactions using stolen credit card information, to more sophisticated schemes like account takeovers and return fraud. The global nature of eCommerce magnifies its vulnerability, as it allows bad actors to impersonate legitimate customers easily. These fraudsters often use false identities or stolen data to purchase goods and services, which they then resell.

One of the most detrimental impacts of eCommerce fraud is the significant increase in chargebacks. Excessive chargebacks result in direct revenue loss and damage a retailer’s reputation with credit card networks. This can lead to increased processing fees and the potential for the business to be categorized as high-risk, compounding financial strain and operational challenges.

Here, we delve into six common types of eCommerce fraud, from transaction fraud to chargebacks, and offer actionable advice on protective measures. By understanding these threats and employing the latest technologies and best practices, retailers can effectively safeguard their business.

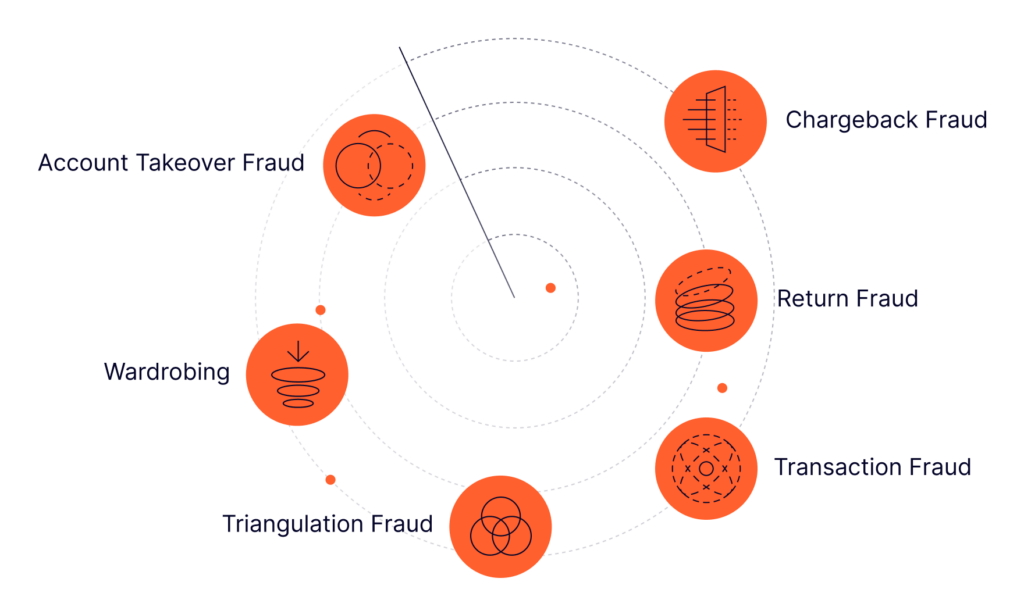

6 Types of Ecommerce Fraud

Here are six examples of how fraudsters may target your eCommerce store to exploit it:

1. Transaction Fraud

Transaction fraud, often called credit card fraud or payment fraud, occurs when malicious actors use stolen credit card information to make unauthorized purchases. In such cases, not only does your business lose the sale, but it may also be compelled to refund the legitimate cardholder if a chargeback is requested.

The repercussions of transaction fraud extend beyond immediate financial loss. An excessive number of chargebacks can categorize your business as a high fraud risk by card networks, resulting in increased processing fees and additional financial burdens. Preventing transaction fraud is crucial to mitigating these costly consequences and maintaining your business’s economic health.

See how SEON’s real-time monitoring prevents fraud, ensures compliance, and unlocks customer insights.

Learn more

2. Chargeback Fraud

Chargeback fraud, also known as friendly fraud or first-party fraud, typically falls into three categories:

- Item Not Received: This occurs when a customer falsely claims they never received the product after it was delivered.

- Item Not as Described: When a customer falsely claims that the item they received was damaged, defective, or not as described to get a refund or replacement.

Innocent or Accidental Requests: These occur when customers do not recognize a purchase on their credit card statement, prompting them to request a refund. - Opportunistic Friendly Fraud: Here, refunds are weaponized by customers who may be dissatisfied or opportunistic. This could stem from disagreement with a store’s policy, such as offering travel credit instead of a cash refund, or simply from buyer’s remorse.

- Malicious Friendly Fraud: In these cases, some buyers plan in advance to commit fraud. They intend to receive an item, falsely claim it never arrived and then request a refund.

Like standard transaction fraud, chargeback fraud results in chargeback fees and shares similar financial repercussions. However, it poses an additional challenge: the merchant must prove the cardholder’s malicious intent when disputing the chargeback, making it particularly complex to resolve.

3. Return Fraud

Return fraud is an escalating issue where fraudsters exploit online stores’ return policies, often in conjunction with transaction fraud. Here are some standard methods they use to deceive online merchants:

- Switch Fraud: Fraudsters purchase a legitimate product online and return a damaged or counterfeit version of the same item.

- Bricking Fraud: Fraudsters buy high-end electronics online, remove valuable internal components (e.g., CPUs, memory cards) and return the now “bricked” item for a refund, exploiting lenient online return policies.

- Open-Box Fraud (Online Return Exploit): Fraudsters return opened items online and repurchase them at a discounted price if the retailer resells open-box items online. Some manipulate return systems to force discounted restocks.

- Reseller or Inventory Depletion Fraud (Online Stock Manipulation): Fraudsters bulk-purchase trending or limited-stock items from online stores, creating artificial scarcity. They resell these products on secondary marketplaces (e.g., Amazon, eBay). Once demand peaks, they return the original unsold bulk purchase for a refund, using the retailer’s return policy without financial loss.

4. Wardrobing

Wardrobing, a pervasive form of return fraud, involves customers purchasing clothing to wear briefly before returning it for a full refund. Originally a challenge primarily for brick-and-mortar stores, this practice has become increasingly common in online shopping, where the impersonal nature of returns – without face-to-face interaction – emboldens more consumers to engage in this behavior. Unfortunately, this fraud can damage merchandise, leading to added expenses for retailers, especially if free shipping on sales/returns is involved.

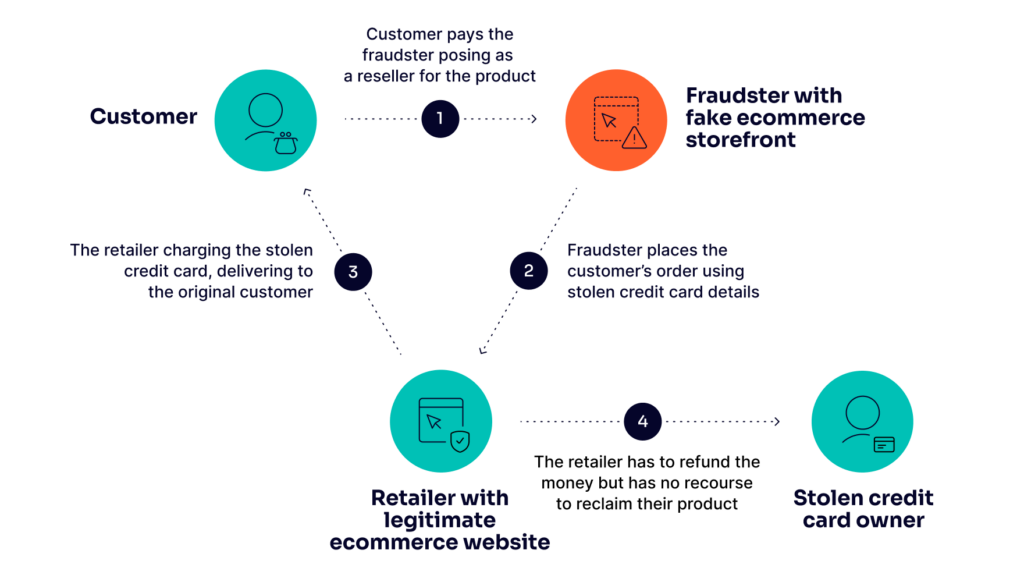

5. Triangulation Fraud

Triangulation fraud is a complex scheme that involves three parties: a legitimate customer, a legitimate online store, and a fraudulent online store operated by a scammer with access to stolen credit card details. Here’s how it unfolds:

- A customer unknowingly places an order with a fraudulent marketplace seller, which might be listed on platforms like eBay or Amazon.

- The fraudster, posing as a legitimate seller, then uses stolen credit card details to purchase the same item from a legitimate online store.

- The legitimate store receives the order with the customer’s shipping address, leading them to ship the product directly to the customer, unaware of the ongoing fraud.

- The customer receives the item, assuming they have purchased it from a legitimate source.

- Eventually, the real cardholder notices the unauthorized transaction and initiates a chargeback.

As a result, the legitimate online store faces the financial burden of the chargeback fee, while the fraudster profits from the customer’s payment and disappears without a trace. This type of fraud effectively victimizes the customer and the business, with the scammer reaping the benefits at their expense.

6. Account Takeover Fraud

Merchant account takeover (ATO) is a serious threat to online businesses, allowing fraudsters to gain access to store admin accounts and exploit them for financial gain. The consequences can include stolen funds, data breaches, and lasting damage to a brand’s reputation. Here’s how these attacks typically unfold:

- Initial Access: Fraudsters gain entry to the store’s admin account using tactics such as phishing to trick employees into revealing login credentials, credential stuffing with leaked or stolen data from breaches, malware or keyloggers to harvest passwords and exploiting weak passwords or vulnerabilities in two-factor authentication (2FA).

- Locking Out the Legitimate Owner: Once inside, attackers secure control by changing login credentials and recovery emails, disabling security notifications and locking out legitimate account owners to prevent detection.

- Manipulating Store Settings: Fraudsters modify key settings, such as replacing the merchant’s payout bank account with one under their control, diverting sales revenue.

- Data Theft and Abuse: Attackers often steal sensitive customer data, including personally identifiable information (PII), payment details, and purchase histories, which can be sold on the dark web or used for further fraud.

- Monetizing the Attack: Finally, they monetize their access by diverting sales funds, selling stolen inventory on secondary marketplaces, or extorting the merchant by demanding a ransom to restore account access.

When your online store enables customers to maintain store credit in their accounts, it effectively transforms these accounts into e-wallets, making them desirable targets for criminals. Account takeover (ATO) fraud represents a critical threat due to its potential as a gateway for further illicit activities.

Once a fraudster successfully gains access to a customer’s account, they can exploit it to commit additional crimes, such as making unauthorized purchases or engaging in identity theft. This type of fraud results in direct financial losses and can significantly damage reputations. Customers whose accounts have been compromised may attribute the breach to inadequate security measures, which can erode trust in your brand.

Explore proactive measures and actionable strategies to combat the most prevalent forms of retail fraud.

Learn more

How to Detect eCommerce Fraud

To effectively combat eCommerce fraud, it’s essential to focus your anti-fraud efforts on three key stages: signups, logins and transactions. Enhancing detection capabilities across these stages requires a multi-faceted approach:

- Leverage Data Analytics: Use data analytics to spot inconsistencies that may signal fraudulent activity. For example, an order placed with a credit card issued in the U.S. but shipped to an overseas location like Croatia should immediately trigger a review.

- Perform Card BIN Lookups: This step is vital in understanding the risks associated with each transaction. A BIN (Bank Identification Number) lookup can confirm the card’s country of registration and whether it’s a prepaid card, which often poses a higher fraud risk.

- Check Digital/Social Footprints: Validate the cardholder’s identity by analyzing their digital footprint. Tools that scrutinize public data from social media or perform email and phone number analysis can provide insights into the user’s legitimacy, enhancing your identity verification processes.

- Identify Card Testing Attempts: Be alert to multiple low-value transactions, especially those under $1, as fraudsters commonly use these to test the functionality of stolen credit card details. Repeated transactions of this nature from a single account should be scrutinized.

- Monitor Connection Methods: Pay close attention to users accessing your platform via VPNs, proxies or emulators. These methods often mask fraudulent activities, indicating potential security risks.

- Assess Shipping Behavior: Implement velocity checks and rules to monitor customer behavior, such as the frequency of purchases and shipping patterns. A high volume of transactions over a short period or multiple failed login attempts can be red flags for fraudulent activities.

- Spot Connections Between Users: Analyze customer data to detect suspicious connections, such as multiple accounts originating from the same IP address or users frequently engaging in promotional abuse. Identifying these links can help you preemptively combat multi-accounting and other typical fraud schemes.

Implementing these strategies effectively requires robust eCommerce fraud prevention software equipped with features like risk scoring, digital footprint analysis, device intelligence, and artificial intelligence (AI) and machine learning (ML). These tools not only enhance your ability to manage risks but also ensure that your anti-fraud measures evolve with the changing dynamics of online threats.

Must-Have eCommerce Fraud Prevention Tools

Fraudsters are constantly evolving their tactics, but with the right tools, online merchants can safeguard their business and customers. Two key technologies stand out for their effectiveness:

- Digital Footprint Analysis: It examines the trail of information that every user online leaves behind, including email addresses, phone numbers and IP addresses, to assess their legitimacy. For instance, it can determine whether an email address is linked to any real social media accounts or is flagged in past data breaches. These insights allow businesses to distinguish between genuine customers and fraudsters attempting to use fake or stolen identities and proactively block suspicious users before they cause harm.

- Device Intelligence: Fraudsters often rely on tools like emulators or virtual private networks (VPNs) to hide their tracks, but device intelligence helps businesses stay one step ahead. This technology analyzes the device being used to make a purchase—whether it’s a phone, tablet, or computer—and detects anomalies in behavior. For instance, it looks at device type, geographic location, and network settings to flag unusual patterns in real time. By doing so, online merchants can stop fraudulent transactions while ensuring legitimate customers enjoy a seamless shopping experience.

Why Machine Learning is Key for Fraud Prevention

Traditional fraud prevention methods, such as blocking specific IP addresses or creating static rules, were once effective. However, fraudsters have grown more sophisticated, finding ways to bypass these outdated defenses. This is where machine learning comes in—a game-changing approach that enables fraud detection to evolve as fast as the threats it faces.

AI-powered tools analyze vast amounts of data to identify suspicious activity. Machine learning models excel at spotting subtle patterns that might otherwise go unnoticed, such as correlations between seemingly unrelated transactions. As fraud tactics change, these systems continuously learn and adapt, ensuring businesses remain protected against emerging threats.

Discover top eCommerce fraud prevention tools of 2025 to protect against chargebacks, account takeovers, and evolving threats while enhancing customer experience.

Read our tool reviews

Comparing Fraud Detection Methods

Here’s how traditional rules-based screening compares to machine learning-based systems:

- Rules-Based Fraud Screening: This approach relies on static rules to detect fraud. For example, a rule might block transactions over $1,000 from certain high-risk countries or flag orders where billing and shipping addresses don’t match. While effective for catching basic fraud, this method has significant limitations. It struggles to identify new or complex fraud tactics and can result in false positives, leading to the rejection of legitimate customers.

- Machine Learning-Based Fraud Screening: Unlike static rules, machine learning uses historical data to detect anomalies and sophisticated fraud techniques. It can identify unusual buying patterns, such as multiple purchases from different accounts originating from the same device. It also uncovers hidden connections between devices, accounts and transactions. Machine learning adapts in real time, enabling businesses to stay ahead of evolving fraud strategies while reducing false declines.

The SEON Advantage

SEON stands out by combining the strengths of custom rules with the adaptability of machine learning. This dual approach enables businesses to stop fraud before it happens while maintaining a smooth and frictionless checkout experience for genuine customers.

As fraud becomes increasingly sophisticated, machine learning is the key to staying ahead. SEON equips you with the tools to protect your business, preserve customer trust, and keep your operations running smoothly. When it comes to fraud prevention, staying proactive is the smartest strategy.

FAQ

Ecommerce and online stores are the targets of transaction fraud attacks (paying with stolen credit card numbers), account takeovers (stealing user accounts), return fraud and more.

Detecting ecommerce fraud starts by logging as much data about customers as possible. It helps to authenticate them at login, spot suspicious information that could point to chargeback fraud, and identify customers who abuse return policies.

Detecting friendly fraud is harder than standard payment fraud. However, fraud detection tools can help you acquire detailed transaction and user data, which will enable you to dispute a chargeback request from an unscrupulous buyer.

The key to preventing ecommerce chargebacks is to create a full profile of your users based on minimal data points and with minimal friction. For instance, an email address could point to a social media profile, which lets you know the person really exists.

You might also be interested in reading about:

- SEON: How to Improve Gift Card Fraud Prevention

- SEON: Best Fraud Detection Software

- SEON: Payment Fraud: How to Detect and Prevent It in Your Business

- SEON: Credit Card Fraud Detection based on Transaction Behavior

Learn more about:

Digital Footprint | Device Intelligence | Device Fingerprinting | Fraud Detection API

Sources

- The Telegraph: Online store fraud rates skyrocket during pandemic